You Can Thank Inflation for the Market Downturn

If you think there’s a lot going on in the markets and economy, you’re not wrong, and you’re not alone.

The market correction so far this year is just one of many expected hiccups that any long-term, diversified investor can and should expect. As such, it’s prudent to stay the course and remain invested in the way your financial plan has outlined.

This long-term thinking doesn’t make the current market shock any less scary. That said, let’s look into what’s driving this craziness in the context of historically similar market cycles.

The Current Landscape

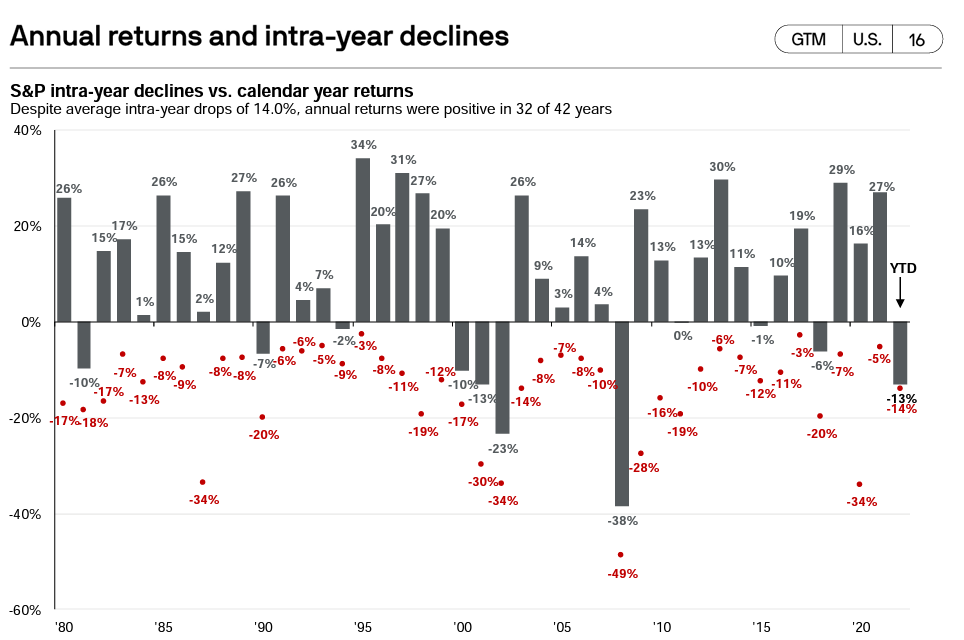

The US stock market has dropped roughly 15% since the start of the year. So how often does this happen? As it turns out, quite frequently. The downturn we’re experiencing now actually happens once per year, on average.

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. Returns are based on price index only and do not include dividends. Intra-year drops refers to the largest market drops from a peak to a trough during the year. For illustrative purposes only. Returns shown are calendar year returns from 1980 to 2021, over which time period the average annual return was 9.4%. Guide to the Markets – U.S. Data are as of May 5, 2022.

So if this sort of market correction is normal, why am I hearing exaggerated claims that this is much worse in the news?

Even though the overall market has fallen roughly 15% this year, the average investor is being hit from all sides, as many sectors have fallen more considerably in recent months, including:

Tech stocks: -21%

FAANG stocks: -38%

Meme stocks (Gamestop, AMC, etc.): -77%

Bitcoin: -50%

Chinese stocks: -47%

Loads of money were flooded into these more speculative stocks in the period following the initial pandemic recovery. When interest rates go up, these speculative sectors tend to get hit the hardest.

The Fed’s Response

Remember, the Federal Reserve (the Fed) increased money supply in order to prop of the economy during the pandemic. It may have saved the economy from free falling, but prices skyrocketed as a result. Look no further than the price of houses, cars, gas, etc.

Now, the Fed is raising interest rates in order to flight inflation, but raising too quickly could teeter the economy into a recession. They have raised interest rates twice so far this year: one increase of 0.25% and a second of 0.50%. They have hinted at raising rates just over 1% for the year, so the hikes are not over yet.

The Fed needs to find a happy middle ground between keeping inflation at bay while also avoiding an economic recession. Talk about pressure… The silver lining is, they’ve done it before, and many think they can do it again.

The Market’s Response

Historically, the stock market tends to recover quite nicely after the Fed raises rates even if the initial market reaction is volatile. In fact, the market finishes positive 100% of the time over the 12 months following a Fed rate hike.

What Should You Do?

While, the fancy charts and graphs don’t make the market-news headlines any less scary, but they certainly justify a long-term, buy-and-hold approach towards investing.

Assuming you’ve built a portfolio that aligns with your time horizon, liquidity needs, tax situation and overall financial plan, the very best thing you can do is nothing at all.

My clients may be sick of me saying, “stay the course,” but I believe this is the best course of action to achieve long-term financial success. Tune out of the media noise, and stick to your plan, and I believe the markets will recover just as they have following every single downturn we’ve ever experienced in the history of the stock market.

If you have taxable assets held in a brokerage or trust account, be sure to harvest losses during this downturn to reduce your lifetime tax bill.

In addition, Series I Bonds—which are now paying 9.62% interest per year—could be a reasonable parking place for excess cash to help curb inflation. You can learn more about Series I Bonds here.

If you want to talk about your long-term investment portfolio, you can reach out to me at Ben@coveplanning.com or schedule a free consultation call.

Sign up for Cove’s Build Your Wealth Newsletter to stay informed with the latest personal finance insights!

Ben Smith is a fee-only financial advisor and CERTIFIED FINANCIAL PLANNER™ (CFP®) Professional with offices in Milwaukee, WI, Evanston, IL and Minneapolis, MN, serving clients virtually across the country. Cove Financial Planning provides comprehensive financial planning and investment management services to individuals and families, regardless of location, with a focus on Socially Responsible Investing (SRI).

Ben acts as a fiduciary for his clients. He does not sell financial products or take commissions. Simply put, he sits on your side of the table and always works in your best interest. Learn more how we can help you Do Well While Doing Good!

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Ben Smith, and all rights are reserved. Read the full Disclaimer.